If your company owns a subsidiary or is a subsidiary of another company, the accounting processes are different from traditional, single-entity accounting.

This is because there are often shared expenses, revenues, and other line items that could bloat the real totals and ultimately land the company in serious legal trouble.

In addition, there isn’t a “one-size-fits-all” accounting method for all subsidiaries.

So in this post, we’ll discuss the different subsidiary accounting methods, when to use them, and how to establish a subsidiary accounting process that is largely automated.

What Is a Subsidiary?

If a parent company owns more than 50% of a company’s voting rights, then the controlled company is considered a subsidiary company of the parent company.

There are two main kinds of subsidiaries:

- Partially owned subsidiaries: The parent company has more than 50% yet less than 100% of the subsidiary’s voting rights.

- Wholly owned subsidiaries: The parent company controls 100% of the subsidiary’s voting rights.

Even though the parent or holding company has significant influence over its subsidiaries, each subsidiary still has its own bank account, tax ID, and accounting processes. So in some ways, it still operates like an independent company. However, there are critical differences in the accounting process for a subsidiary and its holding company.

If the parent company has less than 50% of the voting power, it has some influence over the investee. That being said, it still only owns a minority interest (or noncontrolling interest) in the company. In this case, the company is known as an associate of the parent company rather than a subsidiary. This difference is important for accounting professionals as associates require a different accounting method than subsidiaries.

Accounting Methods for Subsidiaries

The two common accounting methods for subsidiaries include:

Below, we’ll discuss each accounting method, when you would use each one, and provide a few examples.

What Is the Consolidation Method of Accounting?

The consolidation accounting method is the required accounting method for audits. It is most commonly used to account for both partially and wholly subsidiaries.

This is because the subsidiary’s finances are recorded on the parent company’s financial statements, though the parent company is also recording its income (or loss) from each separate legal entity.

Therefore, the earnings of a subsidiary could be counted twice. This could significantly inflate the parent company’s earnings and misrepresent its true financial status.

For this reason, a core aspect of the consolidation method of accounting is intercompany eliminations. This ensures that a subsidiary’s gains or losses are accurately represented in the parent company’s financial statements.

Below we’ll walk through a few examples of the consolidation method in action, or you can read our full guide on consolidated financial statements.

Example of the Consolidation Method of Accounting

You can either perform the consolidation process manually or automate it with software. We’ll start by showing you how to manually consolidate entries and then show you how you can automate it.

Manual Example of Executing the Consolidation Method of Accounting

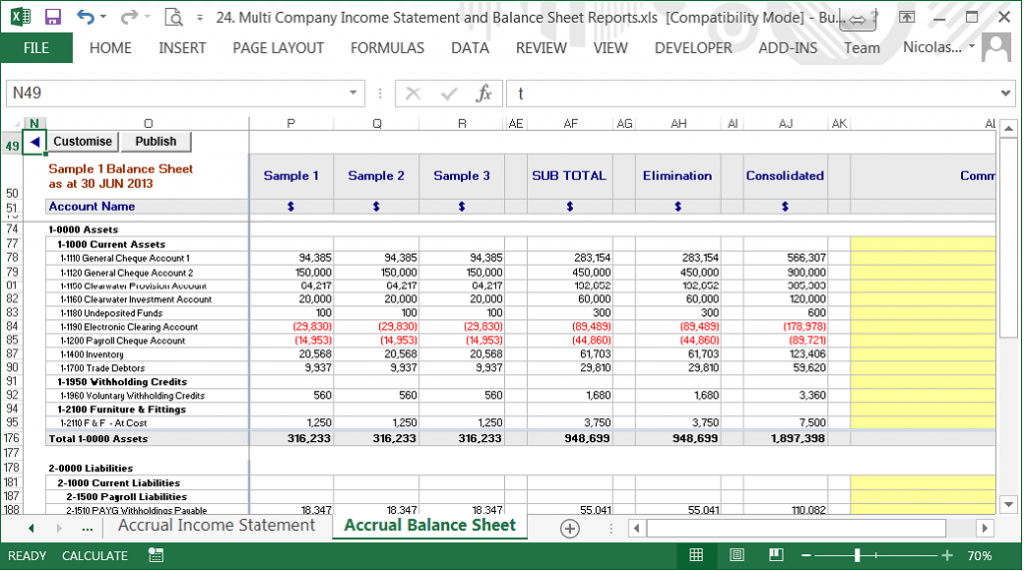

To manually consolidate your financial statements, the first step is to match the subsidiaries’ fiscal periods with the parent company’s fiscal periods.

Once they are aligned, create an Excel spreadsheet with the following labels; liabilities, assets, income, equity, expenses, and cash flow.

Next, copy and paste the data from each subsidiary into the appropriate tab. Be sure to double-check that all of the information is correct, as any inaccurate data could throw off the entire balance sheet.

Finally, perform the intercompany eliminations (eliminating receivables and payables between subsidiaries) and consolidate the data.

Automated Example of Executing the Consolidation Method of Accounting

You can probably execute the consolidation process manually if the parent company only has one subsidiary. However, larger companies with many subsidiaries often need to leverage automation to close the books on time and ensure the data is accurate.

Therefore, here’s an example of what it looks like when you automatically consolidate subsidiaries in SoftLedger.

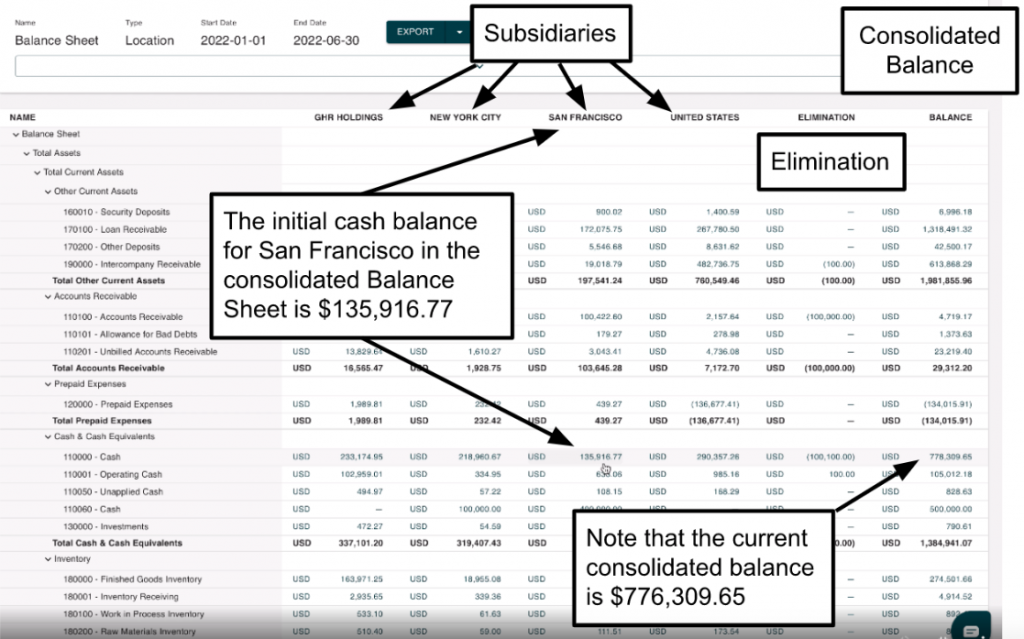

First, you’ll see a consolidated balance sheet along with each of the subsidiaries’ individual balances.

Note here that the initial cash balance for the subsidiary named “San Francisco” is $135,916.77, and the total consolidated cash balance for the parent company is $776,309.65.

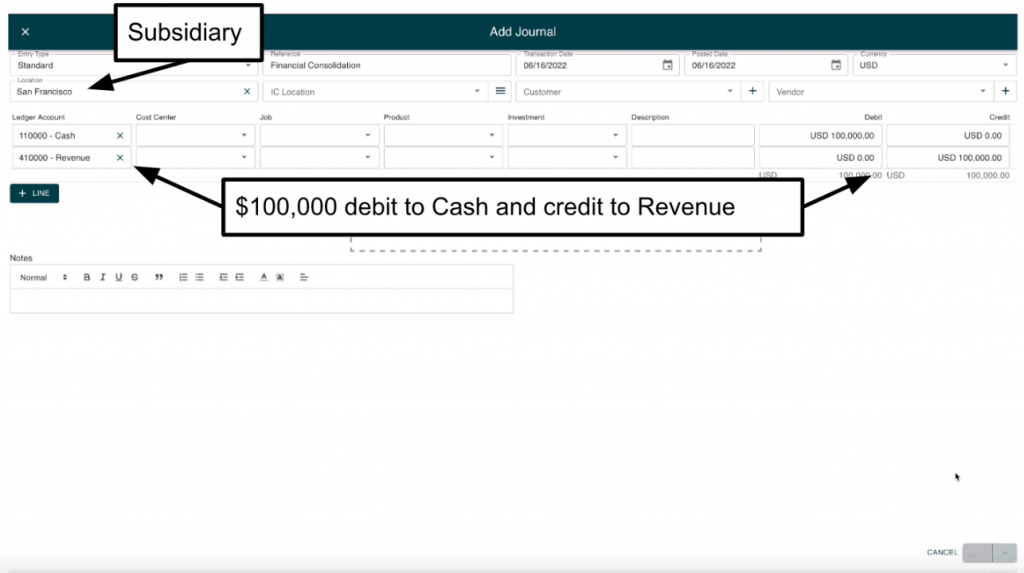

Now, let’s say that the subsidiary San Francisco receives a payment of $100,000. You can enter that journal entry like this:

Then, all you have to do is click “submit” on the journal entry page, and SoftLedger automatically:

- Adjusts San Francisco’s balance

- Performs intercompany eliminations

- Adjusts the consolidated balance sheet to reflect the impact of San Francisco’s latest journal entry.

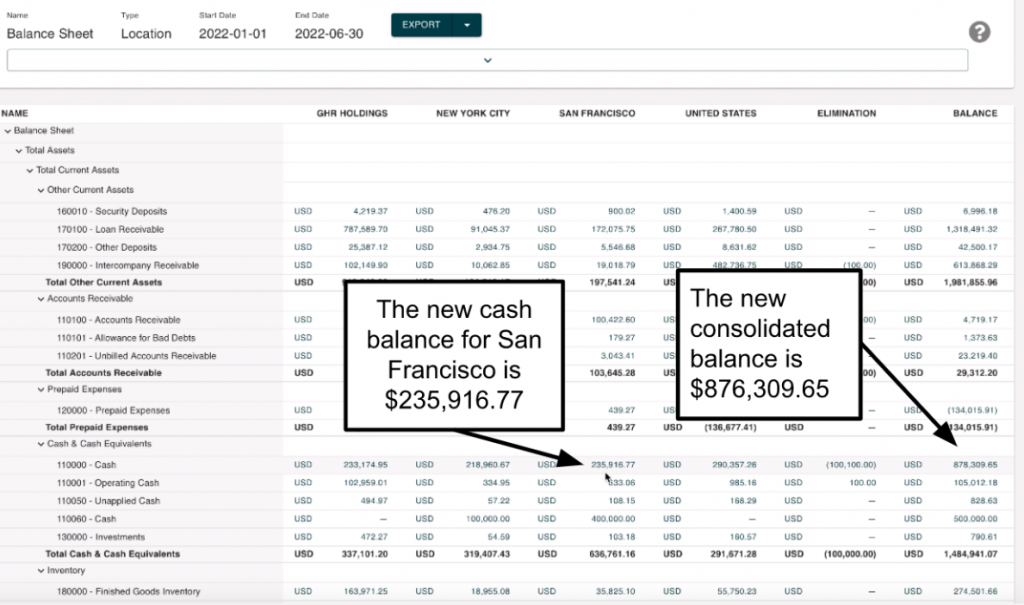

So when you navigate back to the consolidated balance sheet, you’ll see the following up-to-date consolidated balance sheet:

That’s it! You don’t have to calculate anything or manually perform eliminations. This not only makes your data more accurate but also helps your team close the month faster.

What Is The Equity Method of Accounting?

The equity method is generally used by companies that hold between 20% and 50% of the voting power. So it’s normally reserved for holding companies with significant influence over an associate, but there are scenarios where holding companies use it to account for their subsidiaries.

However, it’s important to note that the equity method often is not acceptable for audited subsidiary financial statements.

So how does the equity method work?

In short, the parent company records its share of a subsidiary’s net profit or loss on its non-consolidated income statement.

Example of the Equity Method of Accounting

To help you visualize this concept, here is a brief example.

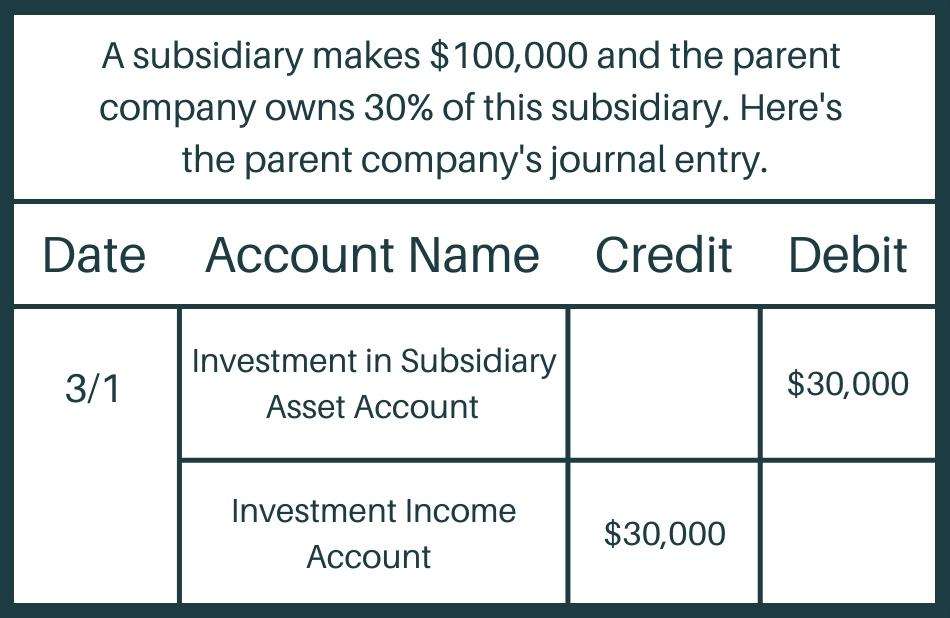

For example, if the subsidiary makes $100,000 and the parent company owns 30% of it, the parent company would record $30,000 in net income on its non-consolidated income statement.

In this case, the holding company would record a $30,000 debit to the Investment in Subsidiary Asset Account and a $30,000 credit to its Investment Income Account.

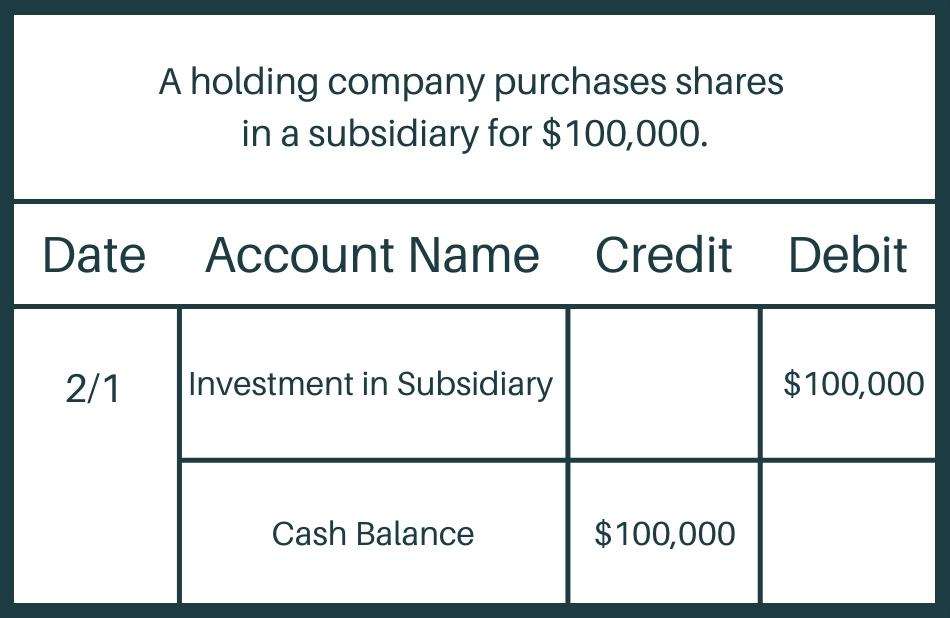

However, when a parent company initially acquires a portion of a subsidiary, it debits Investment in Subsidiary by the purchase amount and then credits cash by the purchase amount.

For example, if the holding company purchased its share in the subsidiary for $100,000, this is what the entry would look like for the acquirer:

The Best Software for Subsidiary Accounting

We built SoftLedger because we couldn’t find accounting software designed specifically for multi-entity companies that needed accurate, real-time data.

So while plenty of different accounting solutions offer consolidation and intercompany elimination add-ons, SoftLedger is unique in that it seamlessly executes the entire consolidation process for you so that the team always has access to an up-to-date balance sheet.

This saves your team time as you no longer have to spend time manually consolidating data and performing intercompany eliminations. In addition, it eliminates room for human error, which improves financial reporting accuracy and ensures the executive team always has real-time data to make better investment decisions.

To see for yourself how SoftLedger can help you improve your company’s efficiency, schedule a demo today!